All About Singapore Company's Offshore Tax

-

Jenny Pham

Singapore's tax system is designed to foster a vibrant business environment and attract global investments. With a reputation for being business-friendly, Singapore offers one of the low corporate tax rates in the region,with a lot of incentives for businesses, for both onshore and offshore companies. Singapore tax mechanisms vary with Corporate Income Tax (CIT), CIT Rebates/tax return, tax exemption schemes for new start-ups, tax incentives for pioneer industries, and international agreements for double taxations. If you want to open Singapore company, the information below will provide you a thorough view on the Singapore corporate tax.

1. Corporate income tax in singapore(CIT)

Singapore corporate tax rate is capped at 17% based on chargeable income/profits of the company. This applies to both local and offshore companies in Singapore.

2. Tax return in Singapore (Corporation Income Tax Rebate or CIT Rebate)

When considering Singapore company registration, all businesses need to be aware of the tax return, also known as CIT rebate, which is one of the major benefits for Singapore companies. The CIT Rebate will apply to the corporate income tax.

All companies, both onshore companies and offshore companies in Singapore, that complete their tax responsibility will receive a tax return as follow:

Companies have employed at least one local employee, pay salary (Singapore Citizen or Permanent Resident, not include the shareholder) in 2023

- If CIT Rebate ≤ $2,000, receives CIT Rebate Cash Grant of $2,000, no other rebates.

- If CIT Rebate > $2,000, receives CIT Rebate Cash Grant of $2,000 + CIT Rebate 50% of chargeable income (maximum of 40,000 USD after minus the CIT Rebate Cash Grant of $2,000)

If companies do not have local employees, they can not receive CIT Rebate Cash Grant of $2,000 but they can still receive CIT Rebate 50% of chargeable income (maximum of 40,000 USD), apply for both Singapore onshore and Singapore offshore companies.

Details and example here: https://www.iras.gov.sg/taxes/corporate-income-tax/basics-of-corporate-income-tax/corporate-income-tax-rate-rebates-and-tax-exemption-schemes

3. Tax exemption schemes for Singapore companies

Singapore has established Start-up Tax Exemption schemes and the Partial Tax Exemption schemes for qualified Singapore companies. These schemes can help reduce the payable tax of a Singaporean company. However, they mainly support local businesses, not the offshore companies.

The tax exemption scheme for new start-up companies in Singapore.

The Start-up Tax Exemption schemes apply to qualifying companies only for their first 3 years of assessment as follow:

- 75% exemption on the first 100,000 SGD of chargeable income;

- 50% exemption on the next 100,000 SGD of chargeable income.

- The maximum exemption for each year is $125,000 ($75,000 + $50,000) for an income of 200,000 SGD.

The partial tax exemption scheme for Singapore company since the 4th year

From the fourth year of assessment onwards, these companies can apply for the partial tax exemption scheme. The amount is as follows:

- 75% exemption on the first 10,000 SGD of chargeable income;

- 50% exemption on the next 190,000 SGD of chargeable income;

- The maximum exemption for each year of assessment is $102,500 ($7,500 + $95,000) for the total of 200,000 SGD income.

However, not all companies can apply for the tax exemption scheme, only onshore qualified businesses can apply for these schemes. Offshore companies with no local office and employee can not apply for tax exemption schemes.

Requirements to apply for tax exemption schemes in Singapore:

All start-up companies can apply for the tax exemption scheme, except:

- Its business activities mainly relate to investment holding

- It takes part in property development for sale, investment, or both

The start-up company must also qualify for the following requirement:

- Be incorporated in Singapore

- Be a tax resident of Singapore for that year of assessment, which means that the control and management of its business was done inside Singapore

- Full control and operates within Singapore

- Holds annual meetings in Singapore and records the minutes of the meetings with at least 50% of the authorized directors present in Singapore during the meetings or the chairman of the Board of Directors is physically in Singapore during the meeting.

- Key employees and managers operating in Singapore

- Has a local office in Singapore

- Have its total share capital beneficially held directly by no more than 20 shareholders throughout the basis period for that year of assessment:

- All the shareholders are individuals; or

- At least 1 shareholder is an individual that has at least 10% of the issued ordinary shares of the company

The final decision on whether the company is eligible for this tax exemption policy in Singapore will depend on the IRAS government in Singapore after reviewing the documents, records and actual situation of the company. Other conditions might be required by the government on a case-by-case basis.

4. Tax incentives in Singapore

Singapore offers various tax incentives to promote specific industries and activities that are considered PIONEER INDUSTRIES include:

- Financial services;

- Bankings;

- Fund management;

- Family offices;

- Insurance and reinsurance business;

- Tourism;

- Shipping and maritime;

- Global trading industries;

- Processing services;

- Research and development;

- Headquarter activities;

- Legal firms;

- E-commerce; and

- Event organization like trade fairs, trade exhibitions, trade missions or to maintenance of overseas trade office

Offshore companies that are established in Singapore can seek suitable tax incentives for their growing business. These incentives vary depending on the business nature of the company.

5. Double tax agreement for international companies in Singapore

Singapore has Double Tax Agreements (DTAs) with 98 countries. With DTAs, companies, especially offshore companies, can claim a double tax deduction for certain types of income, reducing their overall tax liability. Offshore companies that conduct cross-border operations benefit from these DTAs as it allows them to mitigate the risk of being taxed in multiple jurisdictions, which supports the benefits of setting up a company in Singapore.

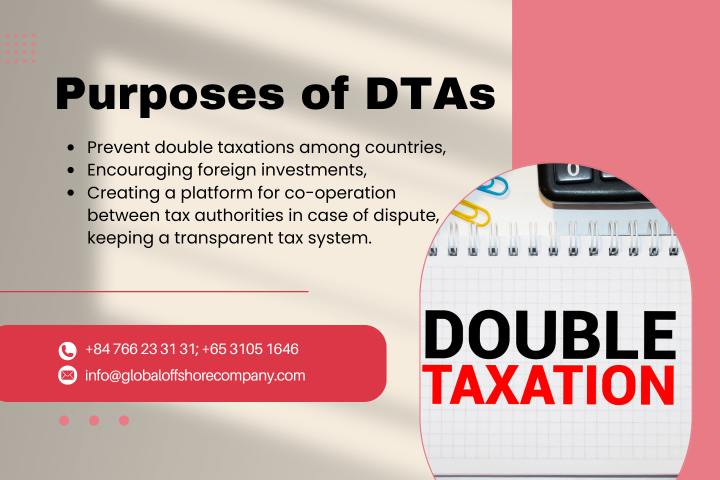

DTAs are implemented for the following purposes:

- Prevent double taxations among countries,

- Encouraging foreign investments,

- Creating a platform for co-operation between tax authorities in case of dispute, keeping a transparent tax system.

Offshore companies in Singapore can benefit from the terms of the DTA between Singapore and other countries. The basic terms in DTA include:

- Classifying which type of income will be taxed in which country.

- The income shall be taxable only in one jurisdiction

- The income may also be taxed in the other jurisdiction but the tax shall not exceed a specified rate (may vary depending on the specific country).

- The income may be taxed in one jurisdiction, and may also be taxed in the other jurisdiction according to the agreement.

- The Residence State provides tax relief for the tax paid in the Source State (as specified in the DTA) to eliminate double taxation;

To mitigate the double tax situation, many countries including Singapore established Double Taxation Agreements (DTAs) that allocate taxing rights, provide relief through tax credits or exemptions, and often reduce withholding tax rates on certain payments. Understanding double taxation is crucial for ensuring compliance with tax laws across jurisdictions, aiding in financial planning and investment decisions, and ultimately reducing the overall tax burden for individuals and offshore businesses engaged in international activities.

CONCLUSION

In conclusion, Singapore's tax framework is strategically structured to promote economic activity and attract foreign investment. By offering competitive corporate tax rates, generous rebates, and targeted incentives, the government not only supports local businesses but also supports offshore companies. The commitment to reducing the tax burden through mechanisms like double taxation agreements further enhances its appeal, ensuring that both local and international companies can thrive in a fair and efficient tax environment for international business growth.

Disclaimer

The information provided in this overview is for general informational purposes only and should not be considered legal, tax or financial advice. While efforts have been made to ensure the accuracy of the content, tax laws and regulations may change. It is recommended that individuals and businesses consult with a qualified tax professional or legal advisor for specific guidance tailored to their circumstances.

Contact Global Offshore Company to set up your Singapore offshore company today!

- Email: info@globaloffshorecompany.com

- Phone: +84 766 23 31 31; +65 3105 1646